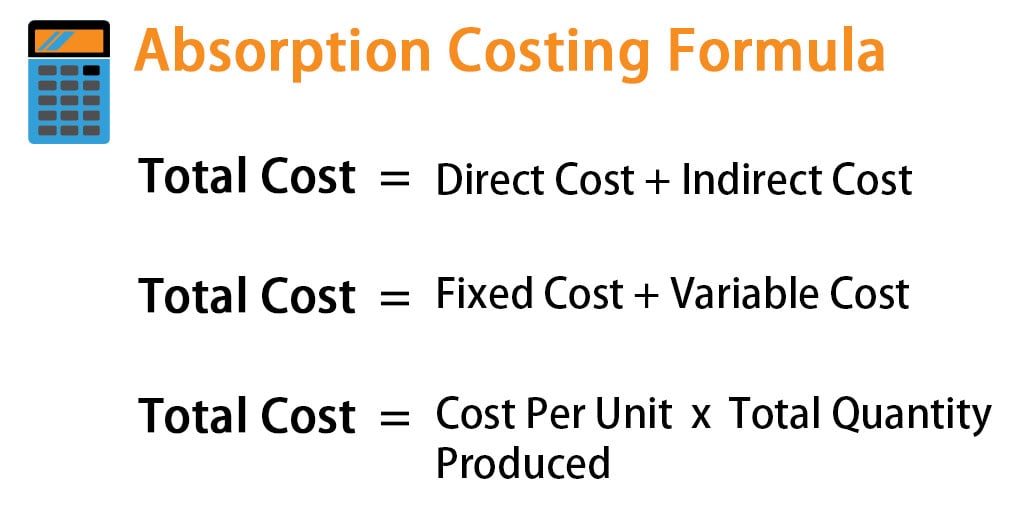

How Do You Calculate Overhead Absorption Rate. the overhead absorption rate is calculated to include the overhead in the cost of production of goods and services. The allocation base is a measure of the activity that drives the indirect costs. Overhead absorption rate = total budgeted overheads / total budgeted activity level. absorption rates can take several forms and follow this general formula: overhead absorption rate = total overhead cost ÷ total units of the allocation base. Absorption rate = (overhead costs / chosen allocation base) x 100. These might differ depending on the type of company. Total budgeted overheads = expected overhead spend. For example, if $50,000 in overhead is “absorbed” by $200,000 in labor costs, this calculation would allocate overhead into wages, as a percentage. the formula for calculating the overhead absorption rate is: It’s used to define the amount to be debited for indirect labor, material, and other indirect expenses for production to the work in progress. Oar = budgeted production overhead / budgeted. Total budgeted activity level = expected number of units produced/services provided. if budgeted output (activity) for the year was 1,000 units, the company could use a fixed production overhead absorption rate (foar) of:

from ximenagokemahoney.blogspot.com

Total budgeted overheads = expected overhead spend. overhead absorption rate = total overhead cost ÷ total units of the allocation base. the formula for calculating the overhead absorption rate is: the overhead absorption rate is calculated to include the overhead in the cost of production of goods and services. Absorption rate = (overhead costs / chosen allocation base) x 100. These might differ depending on the type of company. For example, if $50,000 in overhead is “absorbed” by $200,000 in labor costs, this calculation would allocate overhead into wages, as a percentage. Overhead absorption rate = total budgeted overheads / total budgeted activity level. Total budgeted activity level = expected number of units produced/services provided. Oar = budgeted production overhead / budgeted.

Overhead Absorption Rate Formula

How Do You Calculate Overhead Absorption Rate the formula for calculating the overhead absorption rate is: The allocation base is a measure of the activity that drives the indirect costs. the formula for calculating the overhead absorption rate is: It’s used to define the amount to be debited for indirect labor, material, and other indirect expenses for production to the work in progress. the overhead absorption rate is calculated to include the overhead in the cost of production of goods and services. if budgeted output (activity) for the year was 1,000 units, the company could use a fixed production overhead absorption rate (foar) of: Overhead absorption rate = total budgeted overheads / total budgeted activity level. Absorption rate = (overhead costs / chosen allocation base) x 100. Total budgeted overheads = expected overhead spend. Total budgeted activity level = expected number of units produced/services provided. For example, if $50,000 in overhead is “absorbed” by $200,000 in labor costs, this calculation would allocate overhead into wages, as a percentage. Oar = budgeted production overhead / budgeted. These might differ depending on the type of company. overhead absorption rate = total overhead cost ÷ total units of the allocation base. absorption rates can take several forms and follow this general formula: